On the basis of what was billed as “strong growth signs” in the eurozone yesterday, I offer an antidote in the shape of bollocks-free reality.

On the basis of what was billed as “strong growth signs” in the eurozone yesterday, I offer an antidote in the shape of bollocks-free reality.

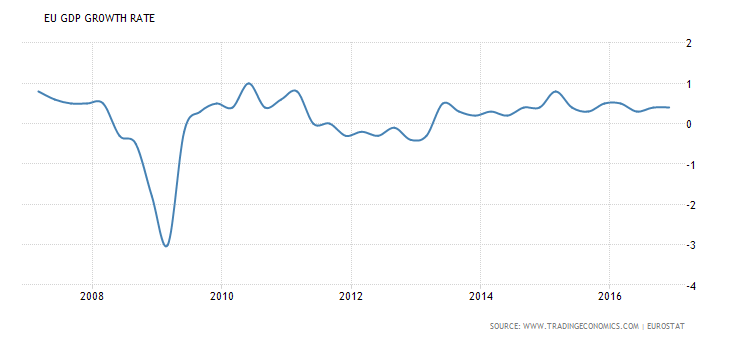

First, let us read between the lines of phrases like “fastest expansion since April 2011”. All things are relative, and in 2011 expansion in the eurozone was far from “fast”. The same caveat applies to the universal use of the word “strong”. This chart shows what a serial flop the eurozone has been in recent years:

You can also see that in April 2011, the zone grew precisely, er, 0.1%.

Secondly, I hate to labour this point again, but PMI research is a measure of expectational manufacturing purchases, not sales, or even dispatched goods. It is riddled with flaws, and frequently wrong.

And last but not least, the fact that Germany “boomed to a 71-month high” is high on hyperbole too, but in truth it represents further bad news: the German economy never has been and never will be an accurate indicator of eurozone health. On the contrary, the central, intrinsic problem with the euro is that of one currency with massive growth – and fiscal variations between Nordeuropa and Club Med.

Why have the world’s pro-EU media handed us this “fake news” to take away to the next Twatterati supper party? The reasons are obvious:

- Draghi is poised to reduce the QE levels in euroland, and thus needs a story that suggests “all is now healed”. This is akin to saying a man with cancer can go back to work because we just put a plaster on his knee graze.

- For all kinds of reasons, the closer Mr Damocles’ sword swings around the single currency’s head, the more its supporters need to make it look viable. (On the basis of yesterday’s risible spin, the £ dropped back to €1.15.6)

- The levels of new investment in the eurozone remain pitiful, and far, far below those we saw prior to 2008. To quote from the OECD report on last year:

Governments have not “stepped up” to spend, and the fanatics in the eurogroupe are still practising scorched-earth austerity. The situation as of February this year was worse than it was at the time of the OECD document.

4. A third but closely connected geopolitical factor is now in play: Brexit. Not only have the Junckers demanded a €60bn “severance fee” from the UK (nowhere to be found in Article 50) but they desperately need to give the impression of Britain leaving an all-First Class global cruise, rather than a torpedoed Lusitania. Further, because most people under 40 don’t know anything any more – and the UK Left of all ages has suffered an irreversible attack of delusional hysteria – a future narrative could easily be woven to the effect that Brexit torpedoed an all First Class global cruise. Don’t laugh: they will try it on.

Just to reiterate the profound and complex nature of doo-doo the euronauts are in, Greece is a vassal State simmering with resentment, Italy is an overborrowed economy with massive fiscal and banking problems, Spain has a standoff at national level (albeit eased for the moment) plus a growing secessional movement, Hungary is flatly refusing to join the euro, and dear old France continues to do nothing to solve its endemic national deficit problems.

The French fiscal watchdog auditor here, the Cours des Comptes, warned the Hollande administration last June that its chances of sticking to a 2.7% deficit target were “very uncertain”. By September, the body declared the 2.7 thing very impossible, and declared a 3% target “very uncertain”. Here we are in March, about to elect a new President, and front runner Emmanuel Macron says he is “sticking to the 3% target”. But he is talking about fiscal 2017: in a barely visible sleight of hand, Michel Sapin told the media yesterday that “France has achieved its deficit target, recording a fall of 0.2%”. This is a lie: the target was 2.7%, but France came in at 3.4%.

The government can play national politics, but it cannot evade forever the bile from Wolfie Wheelchair and his tall social services minder Jeroan Dijesslebleom. The fact is that France has missed its euro deficit commitments by a margin of just under 25%. As Macron is promising tax cuts, either he’s lying or Sapin is. Or of course, both of them.

The euro FinMins met five days ago to consider the results. The lack of leaks thus far suggests strongly that, for once, Juncker has succeeded in telling the eurogropers to shutTF up. And sadly, the global media continue to soak up the bollocks. US business titles last night were announcing how France had “narrowly squeaked under its deficit target of 3.3%”, with just one pointing out that it had “narrowly missed” at 3.4%. Both statements were inaccurate.

Another key fact has also been missed by those who follow the “EUNATO at any price” line dictated by George Soros: the real proof that France has a systemic (not deficit) problem lies – as I have predicted for three years – in its growing pool of unemployed. The country claims to have cut its trade deficit, but sources at prefecturial level in private say this is an accountancy result, not empirical reality. That reality is there for all to see: near-permanent sales in the shops, closing shops, syndicalist unrest, and desk research that continues to point up France’s export problems…..sloppy delivery, uncertain quality, and price.

It is salutory to look again at the booming exports into the Western EU from the former Soviet East. The so-called Visegrad countries of Poland, Slovakia, the Czech Republic and Hungary now account for €500bn of exports on that basis. That still half the size of all German exports….but this is a value, not units, measure: Visegrad products are much cheaper than their western equivalents, and frequently much higher quality. The biggest destination for this export growth is…..France. Join up the dots.

I’m sorry if all this strikes some Sloggers as a tad anorak on my part, but it is vital to keep on pushing against the overwhelming majority of fake news – which comes not from the Right, but from Establishment/liberal media and the Left. For international currency markets to reduce the “value” of Sterling yesterday on the basis of the tosh put out by US business media, Paris, Brussels and the ECB beggars belief….but believe it we must. And be assured of one thing: these false and misleading data will find their way into anti-Brexit articles, tweets, blogs and parliamentary debating points in the coming months – and they will go largely unchallenged. The despicable practice of high-speed multiple lying in a noisy media environment was first pioneered and then perfected by Messrs Mandelson and Campbell during the period 1995-2006. It is now aped around the world, and nowhere more so than in the European Union.